Read time: 7-8 minutes

Since our inception, Vanguard's prioritized long-term success for its investors through disciplined and low-cost investing. There are four principles that define how investors can achieve that success:

- Goals—Create clear, appropriate investment goals.

- Balance—Keep a balanced and diversified mix of investments.

- Cost—Minimize costs.

- Discipline—Maintain perspective and long-term discipline.

Depending on your goals, cash may help you achieve balance and diversification. So what role could cash play in your investments? Let’s explore.

A framework for considering cash

A common financial planning recommendation is that investors keep at least some cash available for emergencies. Cash is a readily available short-term asset with high liquidity, lower market risk, and a short maturity period.

Some investors may wish to include cash in their investment portfolios. “Our approach to assessing how much cash might be appropriate to hold is built on the relationship between an investor’s goals and three critical factors,” said Anatoly Shtekhman, Chartered Financial Analyst (CFA), Head of Advised Portfolio Management Strategies at Vanguard. These factors are:

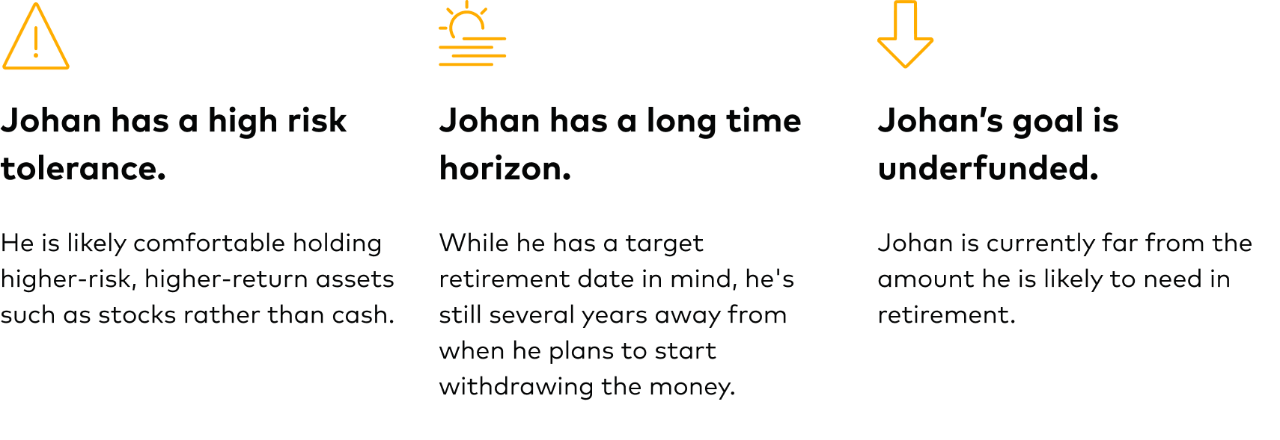

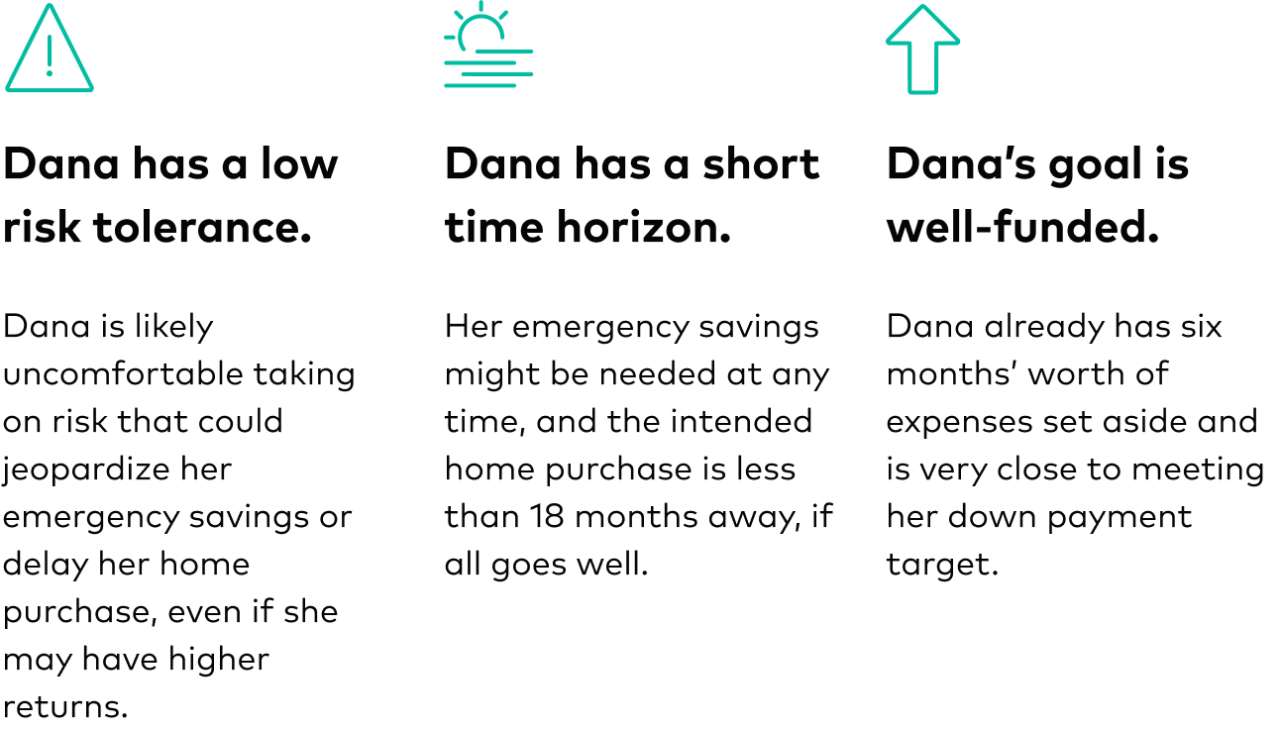

- Risk tolerance—how much market risk an investor is willing to take on. Risk and return are a trade-off. So in many cases, including cash not only moves a portfolio toward the more conservative end of the risk spectrum, it also decreases the chances of providing a high return.

- Time horizon—the length of time an investor can keep their money invested. The shorter that period is, the less likely the investor is to benefit from investing in stocks or bonds. That’s because over the long term, the returns of those riskier assets tend to be higher than those for cash, while over the short term, they tend to be more volatile—and may even lose money.

- Funding level—how close to fully funded a financial goal is. An investor who is close to fully funding their goal may be comfortable having some additional cash available. On the other hand, an investor who is far from reaching their investment goal may be willing to allocate more money to riskier assets for potentially higher returns to improve their chances of success, especially if they have a longer time horizon.

Applying the framework

Johan is in his 50s, and his primary investment goal is funding his retirement.

Dana is just starting out in her career and has two primary financial goals—maintaining her emergency savings and saving for a down payment on a home, which she hopes to buy within the next 18 months.

Dana could think about putting her short-term savings in a few different investments including money market funds (which could be tax exempt) and brokered CDs. She could also consider a cash management account, which is an alternative to a traditional savings account (and typically FDIC insured) but can offer a competitive annual percentage yield compared to savings accounts. To help her maximize her short-term savings, Dana could open a Vanguard Cash Plus Account, a savings account alternative1, which offers a bank sweep with a competitive APY2 and FDIC coverage.3

Dana’s investment choice would be based on her specific circumstances and risk tolerance—picking an investment isn’t one size fits all.

Johan’s and Dana’s framework at a glance

Get help reaching your goals

Explore a Vanguard Cash Plus Account to help you get more from your emergency and short-term savings.

Want to learn more on this topic? Check out:

Whenever you invest, there's a chance you could lose money.

Diversifying means having different types of investments. It doesn’t guarantee you’ll make a profit or that you won’t lose money.

Advisory services are provided by Vanguard Advisers, Inc. (VAI), a registered investment advisor. Eligibility restrictions may apply. VAI cannot guarantee a profit or prevent a loss.

1 Bank savings accounts offer different services and features than a Vanguard Cash Plus Account. For example, savings accounts often offer features like overdraft protection, ATM access, bill pay services and other conveniences that Cash Plus Accounts do not offer. Cash Plus Accounts allow you to hold certain securities that bank savings accounts cannot hold. In addition, Cash Plus Accounts are subject to fraud prevention restrictions such as holding periods and transaction limits, which may not apply to a bank savings account. There may be other differences between these products that you may want to consider before choosing which option is best for you.

2 The bank sweep program annual percentage yield (APY) will vary and may change at any time.

3 Bank Sweep program balances are held at one or more Program Banks, earn a variable rate of interest, and are not securities covered by SIPC. They are not cash balances held by Vanguard Brokerage Services, a division of Vanguard Marketing Corporation (VMC); VMC is not a bank. Balances are eligible for FDIC insurance subject to applicable limits. See the list of participating Program Banks.

The Vanguard Cash Plus Account is a brokerage account offered by Vanguard Brokerage Services, a division of Vanguard Marketing Corporation, member FINRA and SIPC. Under the Sweep Program, Eligible Balances swept to Program Banks are not securities: they are not covered by SIPC, but are eligible for FDIC insurance, subject to applicable limits. Money market funds held in the account are not guaranteed or insured by the FDIC, but are securities eligible for SIPC coverage. See the Vanguard Bank Sweep Products Terms of Use and Program Bank list for more information.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Brokerage assets are held by Vanguard Brokerage Services, a division of Vanguard Marketing Corporation, member FINRA/SIPC.