Read time: 4 to 5 minutes

Deciding when to claim your Social Security benefits is an important decision, and one that may seem a bit overwhelming.

Although you may have heard that you’ll get the biggest benefit if you wait until you’re age 70 to claim, recent Vanguard research, Claiming Social Security early: A spectrum of breakeven and longevity risks, offers a new perspective.

Here’s a quick guide to help you decide if claiming early might be the right move for you:

Who might benefit from early claiming?

- Max savers: If you can rely on withdrawing from a large investment account and aren’t at risk of running out of money, claiming early can be a smart move. It allows you to enjoy your benefits sooner, keep more of your money invested, and potentially leave more to your loved ones or the causes you care about.

- Minimal spenders: If a smaller Social Security benefit could cover low and predictable expenses, you might not need the extra Social Security income later. Claiming early can provide more flexibility and peace of mind.

- Pension holders: If your pension covers all your needs, you might benefit from claiming Social Security early. This can help you preserve your other assets and reduce the need to withdraw from your investment accounts.

- Shorter life expectancy: If you expect to have a shorter life, claiming early can ensure you get the most out of your benefits. It’s important to consider your personal health and life expectancy when making this decision.

“When someone is only using a small part of their investments, they should worry less about running out of money and more about passing away earlier than expected, which creates a need to identify their breakeven point,” said James M. Passman, Vanguard wealth planning methodology analyst and lead author of the research. “For these people, the main goal might be to leave as much as they can to their loved ones or a cherished cause."

Advantages to early claiming

Reducing withdrawals: Claiming early can reduce the amount you need to withdraw from your investment accounts in the first few years of retirement. This can be particularly beneficial if your estate plan involves leaving money for the future and you don't expect to live well into old age.

Tax and Medicare benefits: Claiming early can spread out your tax burden over more years. If your situation benefits from this smoothing, your income taxes and Medicare surcharges may be reduced.

Psychological value: Having cash sooner can provide a sense of security and peace of mind. Although this mindset doesn’t always align with maximizing your wealth and shouldn’t be the primary reason for your decision, for some retirees having immediate access to funds can offer more value.

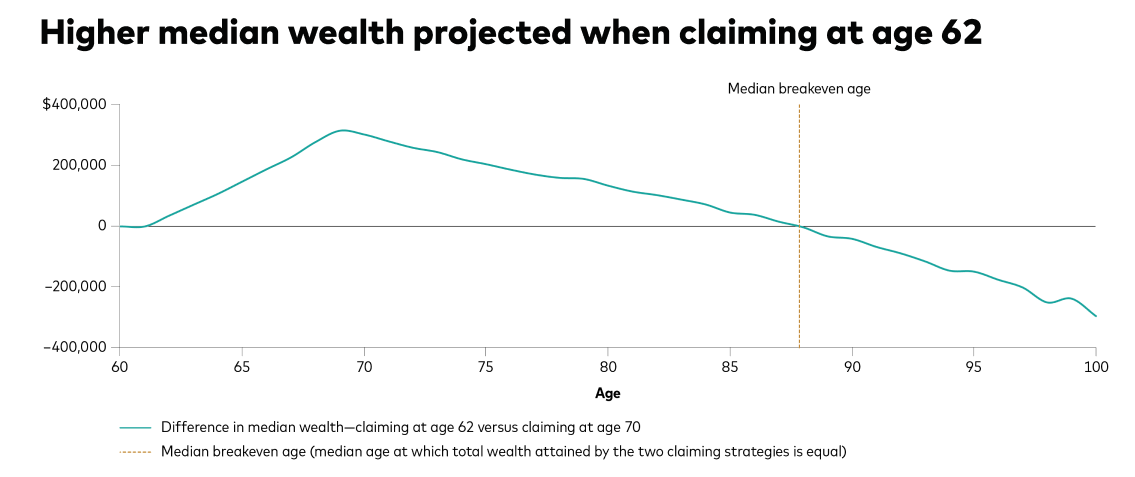

Case studies: Wally and Wanda

Note: Hypothetical case for illustration purposes only. The solid teal line represents the difference in median wealth (claiming at age 62 versus claiming at age 70). The dashed dark yellow line represents the breakeven age (the median age at which total wealth attained by the two claiming strategies is equal). Median wealth is displayed in after-tax, real dollars. Projections are made using the Vanguard Financial Advice Model (VFAM) and Vanguard Capital Markets Model (VCMM). Investment allocation is variable, decreasing in equity weights over time. Any surplus is invested at the target allocation; see Appendix 2 of the research note for more information. State tax is assumed to be 3.07%; 2024 federal tax rates are used. All projections are shown in today’s dollars. For more information on the VFAM, see Appendix 2 of the research note.

Sources: Vanguard calculations, using data from the Society of Actuaries.

IMPORTANT: The projections and other information generated by the VCMM regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Distribution of return outcomes from the VCMM are derived from 10,000 simulations for each modeled asset class. Simulations are as of August 31, 2024. Results from the model may vary with each use and over time. For more information on the VCMM, see Appendix 1 of the research note.

The research also looked at a case study that included Wanda, Wally’s spouse. Five scenarios within the study explore how different claiming strategies could play out in a two-person household depending on factors such as ages, health status, life expectancy, and income.

How you take your Social Security is a highly personal decision, one you should carefully consider based on your circumstances, lifestyle choices, expected cash flows, and understanding how your future needs and wants may differ from today’s. You may want to speak with a financial or tax advisor to see which claiming strategy makes sense for you.

Talk to the pros

Advisory services are provided by Vanguard Advisers, Inc. (VAI), a registered investment advisor. Eligibility restrictions may apply. VAI cannot guarantee a profit or prevent a loss.

The information contained herein does not constitute tax advice and cannot be used by any person to avoid tax penalties that may be imposed under the Internal Revenue Code. Each person should consult an independent tax advisor about their individual situation.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model (VCMM) regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More importantly, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard's primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, U.S. municipal bonds, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over time. Forecasts represent the distribution of geometric returns over different time horizons. Results produced by the tool will vary with each use and over time.

©2025 The Vanguard Group, Inc. All rights reserved.