Read time: 10 to 12 minutes

- Alphabet soup

Medicare options are categorized by letters, like Part A and Part B. They each offer something different, so it's important you know what they involve.

- Key considerations

When choosing coverage, prioritize your needs, evaluate Medicare plan options, and shop for policies.

- What's ahead

Apply for Medicare when you're eligible and review your coverage each year to see if it still matches your needs.

The ABCs of Medicare

Medicare basics

Go by the letters

Before we dig deeper, let’s look at some of the key parts of Medicare and what they involve:

- Part A. Helps cover hospital visits, care at nursing facilities, hospice, and some home health care as well. It’s free for many people.

- Part B. Helps cover doctors’ services, outpatient care, medical supplies, and preventive services. You pay a monthly premium.

- Part C (also called Medicare Advantage): A plan from a private company that’s an alternative to Original Medicare (Parts A and B). Most require use of in-network doctors but may offer extra benefits like vision or dental. Plans have limits on out-of-pocket costs.

- Part D. Helps cover the cost of prescription drugs. This includes many shots and vaccines. It’s a voluntary plan that you pay for. Premiums may be higher if you enroll in this later.

- Medigap. Extra insurance you’d buy from a private company that helps cover costs in the Original Medicare. In most states policies go by letters, like Plan G or Plan K. You can’t have both Medigap and Medicare Advantage.

Keys to coverage

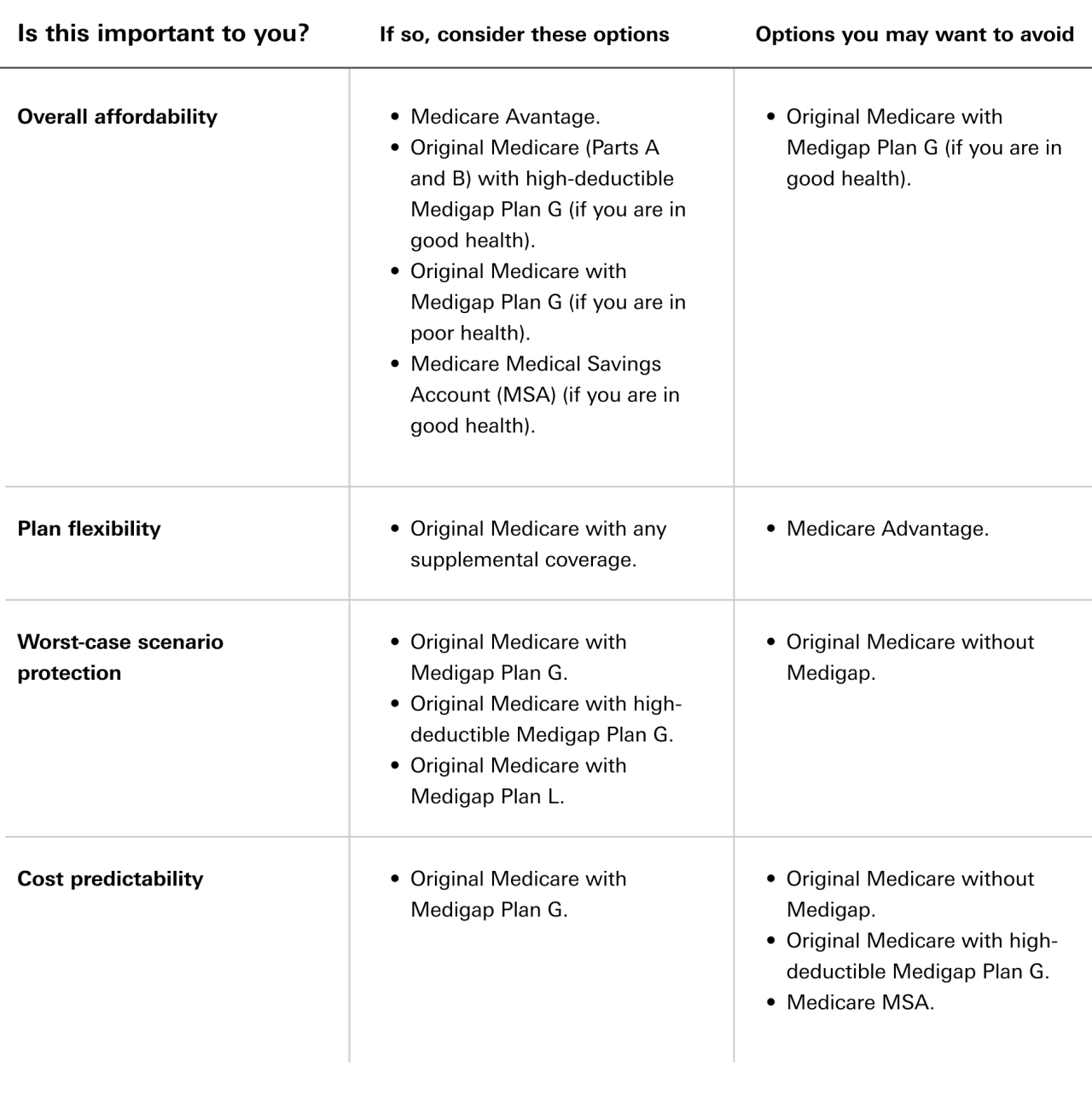

Because health needs are very personal, you’ll need to take a personal approach. Consider these 3 key things when choosing Medicare coverage2:

- Prioritize your needs. What parts of insurance coverage are important to you? You decide what you believe is worth paying for. Consider the tradeoffs—such as affordability, flexibility, and coverage for worst-case scenarios.

- Evaluate Medicare plan options. Find the policy that best fits the plan features that are important to you.

- Shop for policy providers. You’ll likely have several providers to choose from. Shop for the coverage you want and the best deal for where you live.

Fill in the gaps

You might want more coverage than standard Medicare provides. That’s where you can use supplemental insurance called Medigap. This is extra insurance you’d buy from a private company to help cover costs not covered in the Original Medicare. You’ll need to purchase Medigap within 6 months after enrolling in Plan B. There are 10 standard Medigap plans. Click here to learn more.

Tip: Want to get the lowest price? Don’t wait to buy Medigap. If you’re late, you may pay more—or may not be able to get a policy at all.

A deep dive into what Medicare might cost you

Costs can come from:

- Premium. The amount you pay each month to have coverage.

- Deductible. What you pay out of pocket before insurance kicks in.

- Copayments. Fixed amounts that you’ll pay for covered services.

- Coinsurance. A percentage of the healthcare costs you’ll pay.

Here’s a general breakdown, according to Medicare’s website.

Part A—Hospital insurance

- Premium. For most people it’s free, as long as you or a spouse paid Medicare taxes over a long enough time, usually 10 years. If you do not qualify for premium-free Part A, there are monthly premiums. The amount depends on how long you or a spouse worked and paid Medicare taxes.

- Deductible. What you would pay for each hospital stay for each benefit period. The periods will vary depending on when you were admitted and when you last received care.

- Copayments. For inpatient stays, costs change based on how long you’re in a facility. For example, there’s no copayment for days 1 to 60 after you’ve paid your deductible. But copayment costs increase significantly from then on. After 150 days, you pay all costs.

Part B—Medical insurance

- Premium. What you pay can depend on your income. You'll pay a monthly premium even if you don't use the service. Note: If you're enrolled in Social Security, your premiums are deducted from your monthly benefit.

- Deductible. There’s a deductible before Medicare kicks in. This deductible is once per year.

- Coinsurance. Typically 20% of Medicare-covered costs after you’ve met your deductible.

Part C—Medicare Advantage

- Premium. What you pay each month depends on the plan you join. You’ll also need to pay your premium for Plan B to stay in your plan.

- Deductible, copayments, and coinsurance. These will vary based on what plan you’re in.

Note: Plans have limits on your out-of-pocket costs each year.

Part D—Drug coverage

- Premium. This varies based on your plan. Depending on your income, you may have to pay more.

- Deductible. Most plans have a deducible that varies based on the plan.

Note: Your costs depend on your pharmacy, your medicines, and if they’re covered under your plan.

Medigap—Supplemental insurance

So what will I end up paying a year?

A NOTE ON ORIGINAL MEDICARE AND MEDICARE ADVANTAGE

A common question that comes up is—Should I choose Original Medicare and then opt for Medigap, or should I choose Medicare Advantage, which includes supplemental insurance?

There’s no one-size-fits-all answer. Your situation and need will determine if Medicare Advantage makes sense for you, or if you’d get your insurance through Original Medicare (Parts A and B) and then use Medigap to help cover some other costs.

For example: With Original Medicare, you can go to any doctor or hospital that accepts Medicare in the U.S. With Medicare Advantage, you’ll use doctors in your plan’s network (for non-emergencies).* There are other considerations too. With original Medicare, you may want to consider adding Medigap to cover additional expenses. With Medicare Advantage, you won’t need Medigap.

Match your priorities to Medicare policy types

Figure out what’s right for you

Don’t be late to the party

Eligibility for Medicare starts at age 65. Your initial enrollment period is 7 months—3 months before your birth month, your birth month, and then 3 months after. But if you want to start receiving benefits immediately, enroll in the 3 months before your birth month.

No matter what option you choose, don’t be late to enroll. You could have a gap in insurance coverage—which could lead to huge medical bills if something happens to you. And you could face additional premiums for the rest of your life.

Note: You can defer enrollment past age 65, but only if you or your spouse are still working and you have health insurance through an employer. With a deferment, you get a special enrollment period that continues while you work and goes for 8 months after your employment or coverage ends.

ARE YOU RETIRING BEFORE AGE 65?

Going without insurance is a big risk. If you aren’t eligible yet for Medicare, you have options for insurance. If you left your job, you may be able to extend your workplace insurance through COBRA. You can also get insurance through a spouse (subject to employer enrollment rules), a government-sponsored health exchange, or the private insurance marketplace.

To learn more, check out this lesson.

Shop for a policy

Do you know what types of policies you’re interested in? Are you approaching an enrollment period? If so, it’s time to start shopping. Keep a few things in mind:

- Have a full list of your current medications. Different insurers cover different drugs, so have an up-to-date list on hand.

- Coverage choices vary by area. This Medicare tool can help you find the best Part D and Medicare Advantage plans near you. Enter your zip code, your prescriptions, and your pharmacy. You’ll see the costs of different options.

- Policies have different pricing models. Understand how the different polices are rated. Some use your current age, which will increase every year. This could be the least costly option now. But the price could increase rapidly as you get older. Some policies use a price based on the first year you buy it. Prices won’t increase because of age, but they can still increase due to inflation. Others use pricing that applies to everyone—age doesn’t matter.

FREE HELP

These resources may help you:

- State Health Insurance Program. Every state has one. It offers free counseling about Medicare options and rules and can help you with state-specific benefits you might be eligible to receive. Learn more about this program.

- Medicare Savings Programs. You may be eligible to get help from your state to pay for Medicare Part A and Part B through Medicare Savings Programs. You apply through your state, which determines if you’re eligible. Learn more about this program.

Check in on your choices

For current enrollees, the open enrollment for Medicare is from October 15 through December 7 each year. During this time you can check your coverage—especially for prescription drugs—and see if it still makes sense for you. You can change your health and drug coverage during this period each year.

Want to learn more? Check out our article on how to estimate health care costs.

Medicare Q&A

Here are some common Medicare questions and their answers:

Q. When am I eligible?

A. You’re generally eligible to sign up 3 months before you reach age 65. If you’re not yet 65, you may be able to sign up if you have a disability, end-stage renal disease, or ALS (Lou Gehrig’s disease). This site can help you estimate when you’re eligible for Medicare.

Q. How do I sign up?

A. The Social Security Administration handles applications for Medicare. To apply, you can go to a local Social Security office, call them on the phone, or use the online app on their website. Important note: If you're already signed up for Social Security benefits, you will also be automatically enrolled in Medicare Parts A and B if you're not already.

Q. Do I need to sign up if I still have health care coverage through my job (or my spouse does)?

A. That depends. If you don’t have to pay a premium for Part A, you can choose to sign up when you reach age 65 or after. For Part B, you can wait until you or your spouse stop working to sign up, and you won’t pay a penalty for late enrollment. Since there are some exceptions, you can get more information here.

Note: There are some different rules if your health insurance isn’t through a job—like Medicaid, if you are self-employed, or have COBRA coverage.

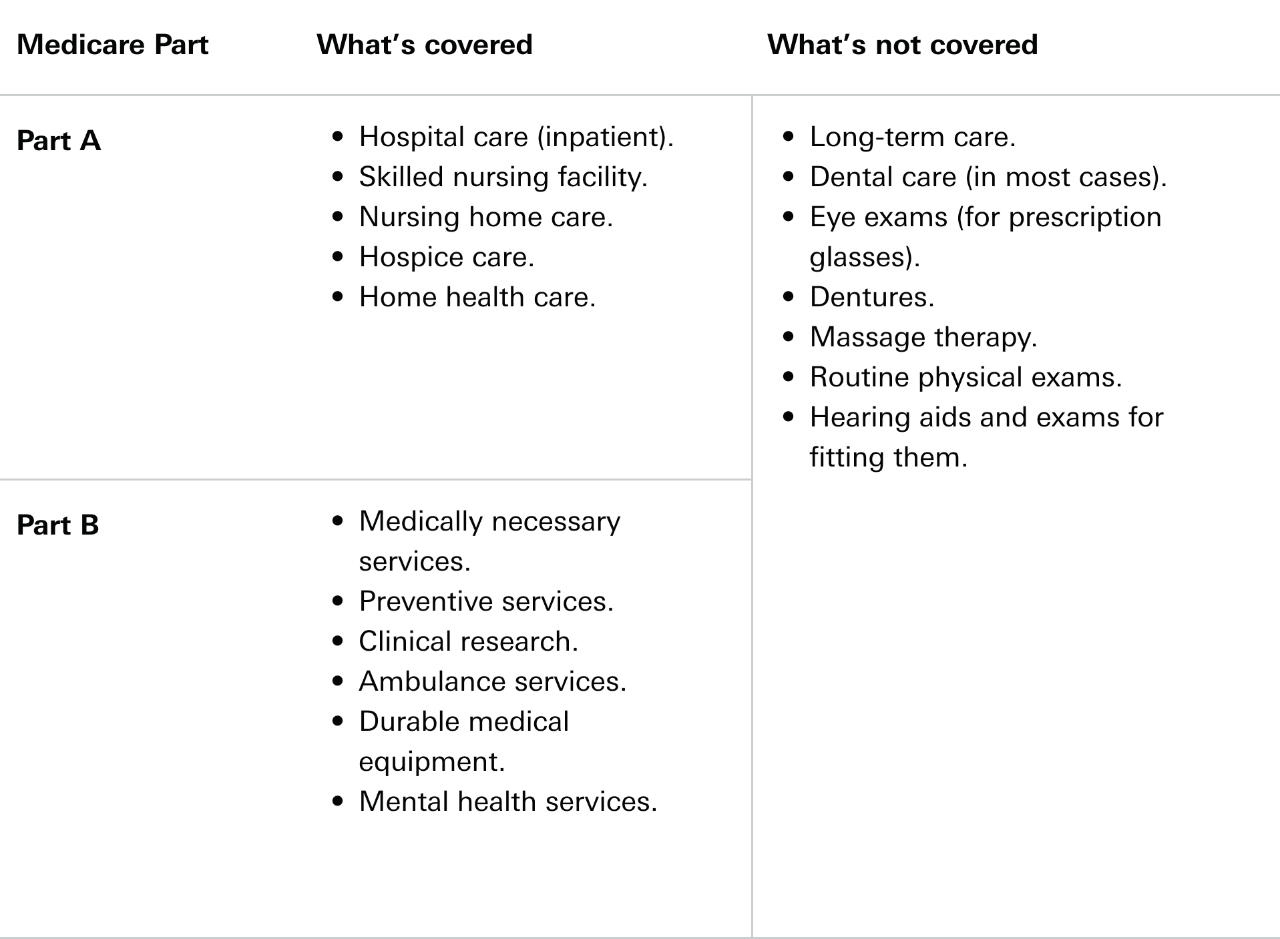

Q. What is and isn’t covered?

A. Here’s a list of some things generally covered and not covered by Parts A and B3:

Note: For Part D, a wide variety of prescription drugs may be covered by the plan, including brand-name and generic drugs. This can vary based on the plan.

Q. Should I choose Original Medicare or Medicare Advantage?

A. That depends on your situation and needs. You’ll have to weigh the pros and cons. For example: With Original Medicare (Parts A and B), you can go to any doctor or hospital that accepts Medicare in the U.S. With Medicare Advantage, you’ll use doctors in your plan’s network (for non-emergencies).4 There are other considerations too. With original Medicare, you may want to consider adding Medigap to cover additional expenses. With Medicare Advantage, you won’t need Medigap.